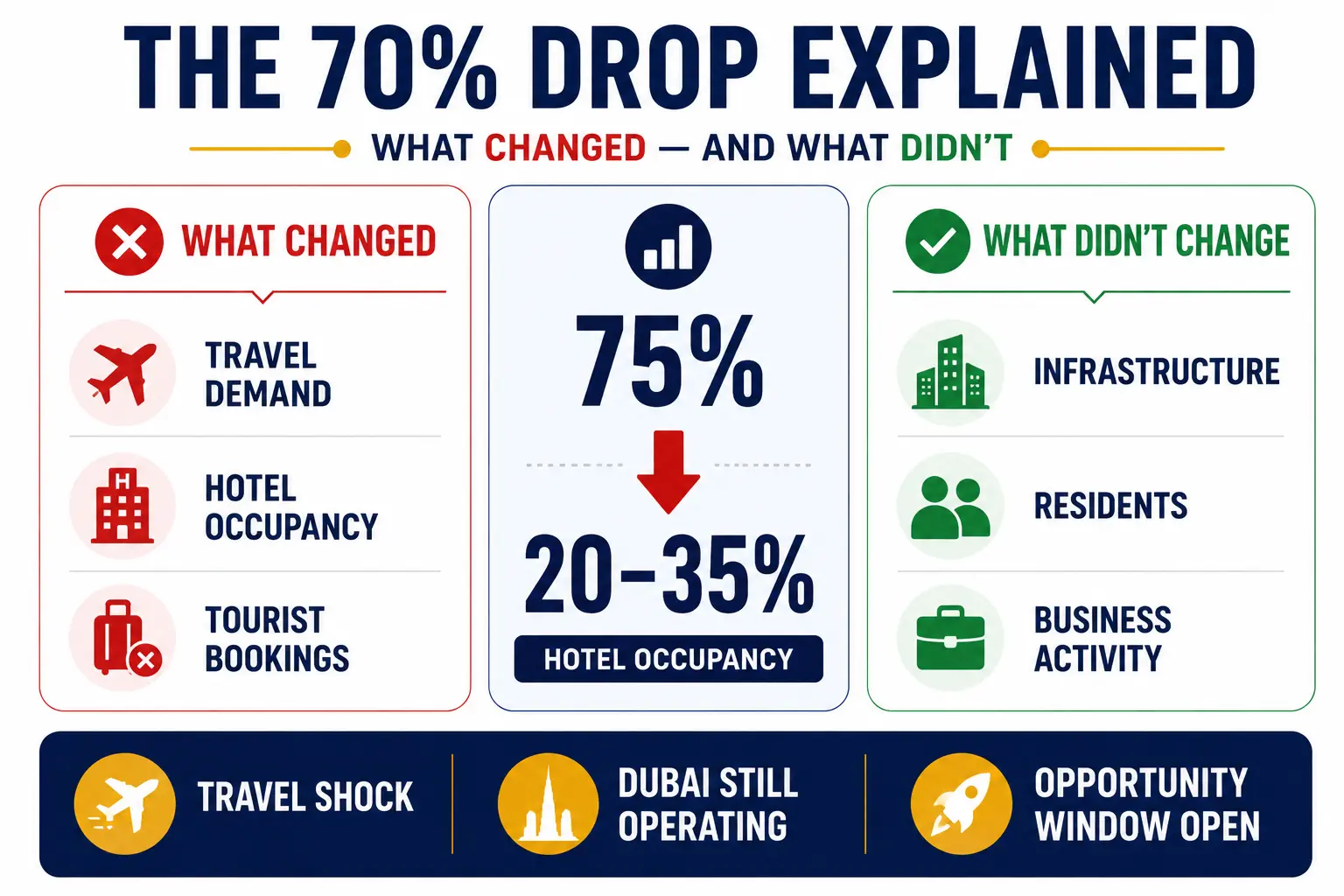

In March 2026, Dubai’s hospitality sector recorded one of the steepest occupancy collapses in its modern history. Hotel occupancy rates fell from a healthy 75 percent in 2024 to just 20 to 35 percent within weeks, a decline of roughly 70 percent from peak levels. Geopolitical tensions triggered by regional conflict led to the near shutdown of Dubai International Airport for several weeks, more than 30,000 flight cancellations, and the immediate loss of over 250,000 short stay bookings across the city.

That 70 percent occupancy drop is the headline number everyone is reacting to with fear. But buried inside that same data are three facts that the most successful hospitality entrepreneurs in Dubai’s history have always understood.

First, hotel real estate lease rates have fallen 15 to 25 percent below 2024 peaks, and landlords who refused to negotiate 18 months ago are now offering free rent months, improvement allowances, and flexible exit clauses. Second, the domestic and corporate hospitality market, which accounts for the majority of revenue in the right business models, has not collapsed at all. Third, Dubai has recovered from every single major crisis in its modern history, and those who launched during the downturn captured market share and cost advantages that persisted for a decade.

This guide is built for founders who are asking the right question: not whether Dubai will recover, but how to position a hospitality business right now to own the market when it does.

Understanding the 70% Drop: What It Means and What It Does Not Mean

The 70 percent occupancy decline is real and serious. But interpreting it correctly is the difference between a founder who panics and a founder who acts intelligently.

Hotel occupancy fell from approximately 75 percent in 2024 to 20 to 35 percent in March 2026. That is a collapse in international leisure and business travel demand caused by a specific geopolitical event: the regional conflict that led to the near-suspension of operations at Dubai International Airport and mass flight cancellations. The disruption is external, event-driven, and temporary.

What has not changed: Dubai’s physical infrastructure is fully intact. Its hotels, restaurants, free zones, roads, financial systems, and regulatory frameworks are all operational. The city’s long-term economic fundamentals, its position as the business hub of the Middle East and Africa region, and its government’s demonstrated commitment to the hospitality sector remain unchanged.

What the 70% Decline Has Actually Created

- Hotel occupancy at 20 to 35 percent means landlords with vacant hospitality properties are losing income every single month. They are now highly motivated to negotiate.

- Real estate lease rates across hospitality-grade properties have fallen 15 to 25 percent below 2024 peaks. Concessions that were unavailable during the boom, including free rent months and tenant improvement allowances, are now standard negotiating outcomes.

- Over 30,000 flight cancellations and 250,000 short-stay cancellations drove expat staff departures, creating a hospitality talent pool that was not accessible 18 months ago.

- Weaker operators who entered the market with thin margins and tourist-dependent revenue are closing, reducing competitive pressure and making market share available.

- The government responded with an AED 1 billion economic incentive package in April 2026 that includes fee deferrals, liquidity support, and business incentive measures specifically targeting hospitality.

The Distinction That Changes Everything

The 70 percent occupancy collapse represents a collapse in international tourist arrivals. It does not represent a collapse in the population of Dubai, the purchasing power of UAE residents, or the corporate demand for furnished accommodation and wellness services.

Approximately 3.5 million people live in Dubai. They are here. They are spending. They want local hospitality experiences, weekend retreats, stress relief services, and quality furnished accommodation. The business models that serve this domestic and corporate market are not experiencing a 70 percent collapse. They are experiencing a demand surge from residents who cannot travel internationally.

This distinction is the entire strategic foundation of a successful 2026 hospitality launch. You are not betting on tourist recovery. You are serving the market that already exists, at costs that are 20 percent lower than they were 18 months ago, with less competition than at any point since 2020.

Historical Evidence: Dubai Recovers Every Time

The 70 percent occupancy decline looks unprecedented to anyone who has not studied Dubai’s hospitality history. It is not. Dubai has faced at least two comparable demand shocks in the past 18 years. Both looked catastrophic at the bottom. Both produced full recoveries within 18 to 36 months. Both created the most significant wealth-building windows in Dubai’s hospitality sector.

Crisis 1: The 2008 Global Financial Crisis

The 2008 collapse was structurally more severe than the 2026 disruption. Real estate values dropped more than 50 percent from peak levels. Construction halted on major projects across the city. International investment stopped. The expat workforce shrank significantly. Tourism collapsed temporarily alongside the broader economic devastation.

Recovery timeline: The bottom was 2008 and 2009. Early stabilisation appeared in 2010. Steady recovery ran from 2010 through 2013. By 2013 and into 2015, Dubai had exceeded pre-crisis highs across every major metric, including real estate, tourism, and business formation.

The wealth creation window was 2008 to 2012. Founders and investors who acquired hospitality assets or locked in long-term leases during that period saw five to ten times returns within seven years. Those who waited for certainty at the bottom entered the market at recovered prices and captured a fraction of the available upside.

Crisis 2: COVID-19 (2020 to 2021)

The COVID shutdown of March 2020 was total and immediate. Tourism stopped overnight. Hotels across Dubai dropped to 20 percent occupancy. The food and beverage industry was devastated. Events and conferences were cancelled indefinitely. Dubai International Airport, which processes more passengers annually than any other airport in the world, fell virtually silent.

Recovery timeline: The free fall ran from March through May 2020. Stabilisation built from June through November 2020. Recovery began in December 2020 and accelerated sharply through mid 2021. By late 2021, Dubai was posting record international tourist arrivals, outperforming every comparable global city.

The speed of the COVID recovery surprised analysts across the industry. Pent-up demand, Dubai’s positioning as a neutral travel destination, and rapid vaccine rollout created a compressed recovery curve. Founders who launched staycation concepts, wellness retreats, ghost kitchens, and tech-enabled hospitality services in mid 2020 entered the recovery with 18 months of reviews, established customer relationships, and lease costs locked at crisis-level rates. Competitors entering in 2022 paid 40 percent more for equivalent properties and had no existing brand equity.

Crisis 3: The 2026 Geopolitical Disruption

The 2026 crisis is structurally closer to COVID than to 2008. There is no underlying economic collapse, no burst property bubble, and no systemic breakdown in Dubai’s financial or business environment. The disruption is on the demand side: international visitors stopped arriving temporarily due to regional conflict and the resulting flight disruptions.

This structural difference is why analysts and hospitality industry observers are projecting an 18 to 24-month recovery, faster than 2008 and comparable to the COVID recovery pace. GCC regional travel is expected to normalise first, followed by broader international visitors as flight schedules return to normal and confidence rebuilds.

| Crisis | Type of Shock | Occupancy Impact | Recovery Timeline | Wealth Window |

| 2008 Financial Crisis | Structural economic collapse | Severe, part of broader collapse | 5 to 7 years | 2008 to 2012 |

| COVID-19 (2020) | Demand shock, total tourism freeze | Down to 20 percent | 18 months | 2020 to 2021 |

| 2026 Geopolitical | Demand shock, flight disruptions | Down 70 percent to 20 to 35 percent | 18 to 24 months (projected) | Now through late 2027 |

The Four Time-Limited Advantages of the 70% Down Market

The case for acting in 2026 is not built on optimism about Dubai’s recovery. It is built on four specific, measurable advantages that exist right now and close progressively as the recovery builds. Every month of delay reduces each one.

Advantage 1: Real Estate Costs Are at Their Lowest Point in Years

Hospitality grade property lease rates across Dubai are currently 15 to 25 percent below their 2024 peak levels. This is a direct consequence of the 70 percent occupancy collapse: landlords with vacant properties are generating zero income, and a long-term tenant at a discounted rate is always preferable to ongoing vacancy.

The strategic value of this discount is not just the monthly savings. A five-year lease signed at 2026 rates locks in that cost advantage for the entire recovery period and well into the growth phase that follows. A competitor launching in 2028 at recovered rates faces a structural cost disadvantage on every operational month for years, regardless of how well capitalised they are.

Example

A hospitality villa in Dubai Hills that was leased at AED 15,000 per month in 2024 is available at AED 11,500 to 12,000 today. Over a five-year lease term, the savings compared to a 2028 competitor paying AED 16,000 per month at recovered rates are AED 216,000 to 270,000 in rent alone, before improvement allowances and free rent months.

Beyond the base rate, landlords are currently offering concessions that were entirely unavailable in 2024: one to two months of free rent at lease commencement, tenant improvement allowances of AED 20,000 to 50,000, flexible break clauses at month 18 or 24, and options to renew at fixed rates. These terms represent additional value on top of the base rate discount.

elementor-template id=”51230″

Advantage 2: The Hospitality Talent Market Has Flipped in Your Favour

In 2024, experienced hospitality professionals were in short supply and commanded premium compensation packages. The 70 percent occupancy collapse changed that completely. Expat staff departures driven by visa uncertainty and the contraction of hospitality employment have created a talent pool that was not accessible 18 months ago.

For a founder launching now, this means access to better candidates at more competitive salary structures, faster hiring timelines, and greater flexibility on contract terms. The quality of the founding team has an outsized impact on the customer experience built during the critical first 12 months, when reviews are earned, and brand reputation is established.

A great team hired at 2026 rates and trained through the downturn, enters the recovery as a highly experienced unit. Competitors hiring in 2028 at recovered salary levels will be training staff from scratch during the period when your team is already fully optimised.

Advantage 3: Suppliers Are Competing for New Business

Food and beverage suppliers, furniture and fixtures vendors, technology service providers, and operational contractors are actively competing for any new hospitality business entering the market. Standard price reductions of 3 to 5 percent below their 2024 rates are now common starting points rather than hard-won negotiating victories.

Extended payment terms, equipment leasing arrangements, and bundled service packages that were unavailable during the 2024 boom are now standard offers. Supply relationships negotiated and formalised in 2026 can be locked into longer-term agreements that extend the cost advantage into the recovery period.

Advantage 4: First Mover Brand Equity Is Only Built in the Downturn

Brand equity in hospitality is accumulated through reviews, repeat guest relationships, and corporate contracts over time. It cannot be purchased or manufactured quickly. A business that opens in mid 2026, builds its review base through the downturn period, and enters 2027 with 12 to 18 months of operational history and a 4.5-plus-star rating across booking platforms has a defensible market position that a 2028 entrant simply cannot replicate.

Corporate clients who sign extended stay contracts or wellness packages during the downturn become the most loyal repeat customers during recovery. Relationships built on reliability and service quality during difficult conditions are significantly stickier than those acquired through promotional pricing in a competitive boom market.

Which Hospitality Models Work When Occupancy Is 70% Down

When overall hotel occupancy is down 70 percent from peak levels, the correct response is not to launch a model that requires those occupancy levels to be profitable. It is to launch a model that generates revenue from the market that exists right now: UAE residents, GCC regional visitors, and corporate clients relocating staff into the stable UAE environment.

Two models meet this requirement clearly. Both can reach break even on domestic and corporate demand alone, without any dependence on international tourist recovery.

Model 1: Staycation and Wellness Retreat

Verdict: Launch Now

The staycation and wellness category is the clearest opportunity in the current market. The 70 percent occupancy decline in traditional hotels has not reduced demand from UAE residents for local hospitality experiences. If anything, it has increased it. Residents who cannot travel internationally are actively seeking quality local alternatives, and the mental health and wellness demand that accompanies geopolitical uncertainty creates additional spending in exactly this category.

Wellness hospitality is counter-cyclical in a way that luxury hotels are not. When people are anxious about regional conflict and cannot fly internationally, they spend more on local stress relief, spa treatments, yoga retreats, and guided wellness programmes. This is the core demand dynamic that makes a 2026 wellness launch not just viable but genuinely well timed.

The Break-Even Advantage at 70% Down

A traditional hotel needs 65 to 70 percent occupancy to cover its cost base, which is exactly the occupancy level that the market does not currently support. A well-structured staycation wellness retreat reaches break-even at 40 to 50 percent occupancy because the revenue per guest is higher through wellness packages, treatments, and experience upsells, the property scale is smaller, and the cost structure is leaner.

This means you can run a profitable operation on domestic demand alone, without waiting for international tourist recovery. When tourists return, and occupancy pushes above 60 to 70 percent, the business moves from sustainable to genuinely profitable. When recovery reaches 80 percent plus in 2027 and 2028, the returns are significant.

Case Study: The COVID Wellness Pivot That Won

When Dubai hotel occupancy hit 20 percent during the COVID lockdown in March 2020, a cohort of hospitality entrepreneurs converted vacant residential properties in JBR and Dubai Marina into wellness-focused staycation retreats targeting UAE residents who could not travel internationally. They locked in 12-month leases at crisis rates, partnered with local yoga and meditation instructors, and marketed through Instagram and LinkedIn corporate channels.

By December 2020, several of these operations had reached 65 percent occupancy, higher than most traditional hotels in the city at that time. By mid 2021, the strongest operators had opened second locations. When international tourism recovered fully in late 2021, they entered the growth phase with 18 months of verified reviews, established corporate wellness contracts, and lease costs locked at COVID-era rates.

Competitors who launched in 2022 paid 40 percent more for equivalent properties, had no existing reviews, and entered a market that had already developed clear brand leaders in the wellness staycation category. The 2026 playbook is structurally identical. The residents are here, the demand is real, and the lease rates are at their lowest in years.

Investment required: AED 500,000 to 1,000,000 Timeline to profitability: 9 to 15 months

Model 2: Extended Stay Serviced Apartments

Verdict: Launch Now

The 70 percent occupancy collapse in traditional hotels has had the paradoxical effect of increasing demand in the extended stay category. As companies relocate team members from conflict adjacent regions into the stable UAE environment, demand for professionally managed, furnished monthly accommodation has become a corporate priority across dozens of multinational organisations.

This is not tourist demand. It is corporate mobility demand, and it is growing precisely because of the geopolitical disruption that is hurting leisure hotels. A company placing 15 employees in furnished serviced apartments for six months generates more predictable, stable revenue than 15 individual tourists booking two-night stays, at lower marketing cost and with natural renewal cycles built into the relationship.

Why This Model Is More Resilient Than Traditional Hotels

Extended stay serviced apartments can achieve 60 to 70 percent occupancy during the current downturn on corporate demand alone. As recovery builds through 2027, the mix of corporate and leisure guests improves, pushing occupancy toward 80 to 85 percent in Year 2 and Year 3. The business is never dependent on the 70 percent occupancy level that is currently unavailable across the broader hotel sector.

Operational complexity is also significantly lower than running a full-service hotel. A 10 to 20-unit serviced apartment operation requires a smaller team, simpler systems, and less infrastructure investment. This makes it an accessible first hospitality business for founders building their operational knowledge base before scaling.

Investment required: AED 750,000 to 1,500,000 Timeline to profitability: 12 to 18 months

Model 3: Medical Tourism Hotel Integration

Verdict: Proceed With Caution

Healthcare demand is resilient, and international patients continue to travel to Dubai for medical procedures regardless of the regional disruption. Post-procedure recovery hospitality is a genuine niche with real demand. However, regulatory complexity, minimum investment above AED 2,000,000, and the requirement for established clinic partnerships make this unsuitable for first-time hospitality founders launching during a crisis period. Better suited to experienced operators with existing medical relationships and UAE regulatory knowledge.

Model 4: Traditional Full Scale Hotels

Verdict: Wait Until Late 2027

With occupancy down 70 percent and international tourism 18 to 24 months from normalisation, launching a traditional hotel in 2026 means absorbing AED 3 to 5 million in first year operating losses. Unless you have 24 or more months of full operating capital and are specifically positioning to scale aggressively during recovery, the traditional hotel launch window opens in late 2027. The exception is founders with exceptional capital reserves who can run sustained losses as a deliberate market positioning strategy.

| Model | Launch Timing | Break Even Occupancy | Revenue Source in 2026 | Primary Risk |

| Staycation and Wellness | Now | 40 to 50 percent | UAE residents, GCC visitors | Small initial scale |

| Extended Stay Apartments | Now | 55 to 65 percent | Corporate relocations | Corporate contract dependency |

| Medical Tourism Hotel | Caution | 50 to 60 percent | International medical patients | Regulatory complexity |

| Traditional Full Hotel | Wait until 2027 | 65 to 70 percent | International tourists | Tourism recovery timeline |

Financial Strategy: Building for the Recovery While Surviving the Downturn

Conservative financial modelling is the single most important discipline for a 2026 hospitality launch. The founders who fail in downturns almost always share one characteristic: they modelled optimistic scenarios and ran out of operating capital before the market turned. The founders who succeed model the conservative scenario and hold cash reserves that allow them to outlast the disruption and capitalise on recovery.

Three Capital Paths

Path 1: Bootstrap Lean (AED 500,000)

Suited to solo founders with strong personal operational capacity who want full ownership and are comfortable running a lean, owner operated model. The priority is speed to market, review accumulation, and proof of concept before adding capital.

- Personal capital: AED 200,000. Business loan or credit facility: AED 300,000.

- Model: Small staycation villa with 5 to 10 guest capacity, run by the founder with one to two part-time staff.

- Month 7 target: break even at 40 to 50 percent occupancy.

- Year 1 revenue projection: AED 250,000 to 350,000.

- Year 2 revenue projection: AED 700,000 to 900,000 as occupancy builds with early recovery signals.

Path 2: Angel Backed Growth (AED 750,000 to 1,000,000)

Suited to founders with strong operational vision who want to launch at a meaningful scale with 18 months of operating runway built in. Angel funding removes the existential risk of running out of cash during the stabilisation period.

- Angel investment: AED 500,000 to 700,000 with a typical 40 to 60 percent equity split.

- Model: Extended stay serviced apartments with 10 to 15 units, a professional team, and a digital booking system.

- Break-even timeline: 14 to 18 months.

- Year 2 revenue projection: AED 900,000 to 1,200,000.

- Year 3 revenue projection: AED 1,500,000 to 2,000,000.

Path 3: Strategic Partnership (AED 1,000,000 or above)

Suited to founders with strong management and marketing skills who want to operate at a premium scale through a capital partnership with an established hotel operator.

- Founder contribution: AED 200,000 to 300,000 plus day-to-day operational management.

- Model: Premium wellness hotel with 50 to 100 room keys, corporate retreat positioning, and wellness centre.

- Break-even timeline: 18 to 24 months.

- Year 3 revenue projection: AED 2,000,000 to 2,500,000.

5 Year Revenue Projection: Staycation Wellness (Conservative Scenario)

| Year | Period | Occupancy Target | Revenue (AED) | Net Position |

| Year 1 | 2026 Crisis Period | 40 to 50 percent | 300,000 to 500,000 | Near breakeven to small loss |

| Year 2 | 2027 Early Recovery | 60 to 70 percent | 800,000 to 1,200,000 | AED 200,000 to 300,000 profit |

| Year 3 | 2028 Full Recovery | 80 percent plus | 1,500,000 to 2,000,000 | AED 600,000 to 800,000 profit |

| Year 4 | 2029 Growth Phase | 85 percent plus | 2,000,000 to 2,500,000 | AED 900,000 to 1,200,000 profit |

| Year 5 | 2030 Market Leader | 85 to 90 percent | 2,500,000 to 3,000,000 plus | Expansion capital available |

The key insight in this projection is that Year 2 and Year 3 are where the crisis-launched business creates disproportionate returns. The cost structure is locked at 2026 rates, the brand equity is established, and corporate relationships are generating recurring revenue, all while competitors who waited are paying 2028 prices for real estate and spending 12 months building the review base you already have.

Pricing Strategy During the 70% Down Period

The most damaging error a 2026 founder can make is aggressively discounting rates to fill occupancy during the downturn. Discount pricing trains the wrong customer segment, creates margin pressure that persists into the recovery, and signals desperation rather than quality positioning.

- Position on guest experience and wellness outcomes, not on nightly rate.

- Create package pricing that bundles treatments, classes, and accommodation into higher value transactions.

- Build corporate contract pricing that offers volume certainty in exchange for modest rate concessions.

- Maintain messaging that signals long term commitment: you are here for the recovery, not offering crisis bargains.

Real Estate Strategy: Locking In the Discount Before It Closes

The real estate decision is the single biggest financial lever in a hospitality business. Getting the lease right in 2026 creates a compounding cost advantage that persists for the full duration of the lease, regardless of what market rates do during the recovery period.

The Long-Term Mathematics of Acting Now

- Scenario A (launch in 2026): Five-year lease signed at AED 12,000 per month. Total lease cost over five years: AED 720,000.

- Scenario B (competitor launches in 2028): Five-year lease at AED 16,000 per month at recovered rates. Total lease cost over the same period: AED 960,000.

- Your structural cost advantage: AED 240,000 in rent savings over five years, before improvement allowances, free rent months, and the brand equity accumulated during the two years your competitor was not yet in the market.

Lease Negotiation Tactics That Work in This Market

Landlords with vacant hospitality properties are under genuine financial pressure right now. Every month a property sits empty is a month of zero income. Use this leverage methodically.

- Open negotiations at 25 to 30 percent below the listed base rate and expect to close at 15 to 20 percent below.

- Request one to two months of free rent structured as a rent holiday at the start of the lease term.

- Negotiate a tenant improvement allowance of AED 20,000 to 50,000 for renovation and fit out costs.

- Push for an option to renew at a fixed rate tied to a consumer price index cap rather than open market rates.

- Include a break clause at month 18 or month 24 to protect against extreme downside scenarios.

- Confirm all utility connections are active and operational before lease commencement to avoid delays.

For business setup and lease structuring guidance specific to UAE hospitality operations, Creation Business Consultants provides detailed frameworks covering mainland and free zone options, trade license categories, and lease negotiation best practices. (Source: creationbc.com)

Month-by-Month Launch Plan for 2026

Pre-Launch: Two Months Before Opening

- Validate your hospitality model choice based on available capital, personal skills, and risk appetite.

- Conduct 10 to 15 direct interviews with UAE residents and corporate potential clients to confirm demand.

- Stress test your revenue model at 40 percent occupancy to confirm the business is sustainable through the downturn.

- Secure your capital source through bootstrap funding, angel investment, or a business loan.

- Prepare a business plan of 5 to 10 pages with three-year financial projections at conservative occupancy assumptions.

- Engage a UAE business setup advisor to confirm the correct licensing pathway and registration structure.

Launch Phase: Months 0 to 3

- Identify your property and negotiate full 2026 discount terms, including base rate reduction, free rent, and improvement allowance.

- Sign a three to five-year lease with a break clause and fixed renewal option.

- Execute renovation and fit out within the tenant improvement allowance budget.

- Hire your core team: one operations manager and two to three hospitality staff members.

- Set up booking systems, payment processing, and guest communications infrastructure.

- File your license application with the relevant Dubai authority.

- Build brand identity, website, and social media presence at least four weeks before your opening date.

- Begin corporate outreach and partnership pipeline before opening, not after.

Growth Phase: Months 3 to 12

- Target 30 to 40 percent occupancy by month three and 45 to 55 percent by month six.

- Gather and respond to customer reviews actively. Target a 4.5 or above rating across all booking platforms.

- Sign at least two to three corporate contracts for extended stay arrangements or regular wellness packages.

- Track repeat customer rate monthly and target 30 percent or above by month nine.

- Identify expansion triggers: when Year 1 occupancy consistently exceeds 60 percent, begin planning the second location.

elementor-template id=”51283″

Competitive Dynamics: Who Is in the Market and Who Is Leaving

Understanding the 2026 competitive landscape prevents both overconfidence and unnecessary fear. The most important thing to understand is that the market is consolidating, and consolidation during a downturn creates conditions that favour well-capitalised new entrants.

The Exit of Weak Operators Creates Space

Operators who entered the Dubai hospitality market in 2023 and 2024 with thin margins, tourist dependent revenue models, and limited operating capital reserves are closing or significantly contracting. Industry estimates suggest 30 to 40 hotel closures in Dubai during the 2026 downturn period. These closures release hospitality real estate back into the market at negotiable rates and reduce competitive density across key submarkets.

Distressed operators also create opportunistic acquisition possibilities. Properties that are already fitted out, have established review histories, and carry existing brand recognition can sometimes be acquired from exiting operators at significant discounts, bypassing the setup phase entirely.

Your Durable Competitive Advantages

- Lease rates locked at 2026 levels give a structural cost advantage over every competitor who launches during or after the recovery period.

- First mover brand equity in the domestic staycation and wellness niche builds through accumulated reviews and repeat guest relationships that later entrants cannot replicate quickly.

- Corporate relationships established during the downturn are stickier and more loyal than those acquired through promotional pricing in a competitive boom environment.

- Operational knowledge built by managing a hospitality business through a difficult period is a genuine capability advantage over founders who only ever operated in boom conditions.

Addressing the Hard Questions About Launching When Occupancy Is 70% Down

What If Recovery Takes Longer Than 24 Months?

This is the right question to ask before committing capital. The most likely scenario is 18 to 24 months. The worst-case reasonable scenario is 36 to 48 months. Your staycation or extended stay model does not require international tourist recovery to reach profitability. It operates on domestic and corporate demand that exists right now and continues regardless of the recovery timeline.

Mitigation: Build your financial model on 40 to 50 percent occupancy at conservative pricing. Ensure 24 months of operating reserves before launch. Diversify revenue across room bookings, wellness treatments, online classes, and corporate contracts so no single stream is critical to the business’s survival.

What If I Choose the Wrong Model?

The wellness staycation model carries the lowest capital requirement and the lowest operational complexity of the viable options. A small villa-based operation can be adjusted relatively quickly if demand signals shift. Launch with a soft opening period, test pricing and packaging with real paying customers, gather direct feedback, and iterate before committing to full scale. Eighteen months of operating runway gives substantial time to optimise based on real market data.

What if better-funded competitors launch later?

First mover advantage in hospitality is real and durable in ways that do not apply in technology or retail sectors. Reviews cannot be manufactured quickly. Corporate relationships take months to build. And lease cost structures locked in 2026 are permanent advantages that later entrants with larger budgets cannot overcome.

A competitor launching in 2028 with AED 5 million in funding still faces real estate costs that are 20 to 25 percent higher than yours, a market that has already been crowded with recovered competitors, and no existing review base or brand equity to leverage. Capital does not substitute for time in the market.

What If I Do Not Have Hospitality Experience?

Staycation wellness and extended stay serviced apartment operations do not require traditional hotel management credentials. The operational complexity is significantly lower than that of a full service hotel. You can hire an experienced hospitality operations manager for AED 5,000 to 8,000 per month, engage a specialist consultant on a monthly retainer for strategic guidance, and build institutional knowledge through Dubai hospitality associations and peer networks.

Leadership clarity, capital discipline, and genuine obsession with the guest experience matter far more in these models than formal hotel management backgrounds. The founders who succeeded in the COVID staycation space in 2020 were not experienced hoteliers. They were agile entrepreneurs who understood their market and built strong teams.

Conclusion

The founders who will look back on 2026 as their defining moment are not waiting for occupancy to recover before they act. They are studying the pattern from 2008 and 2020, understanding the structural difference between a demand shock and an economic collapse, and making the decision that the best time to lock in a 20 percent real estate discount, hire from a deep talent pool, and build first mover brand equity is now.

Two of the three major crises in Dubai’s recent history produced their primary wealth creation windows in precisely these conditions. The founders who launched wellness and staycation concepts during the COVID occupancy collapse in 2020 are the best-positioned hospitality brand owners in Dubai today. The 2026 opportunity is structurally identical, and the 70 percent occupancy drop that is driving fear in the market is creating the same entry conditions that made those founders successful.

The real estate discount is real and time-limited. The talent pool is accessible. The government support is committed. The competitive field is clearing. The domestic market is spending. And the two models that win in this environment generate revenue without requiring international tourist recovery.