Dubai is racing to become the Middle East’s fintech powerhouse. In 2026, the regulatory landscape has fundamentally shifted. The introduction of the Virtual Assets Regulatory Authority (VARA) brought clarity, while the UAE’s 9% corporate tax and zero personal income tax created an unprecedented advantage for startups.

The UAE fintech market is projected to reach USD 52.07 billion by 2026, with Dubai capturing the lion’s share. What was once confusing is now achievable. Whether you’re launching a crypto exchange, blockchain platform, or traditional fintech solution, this guide walks you through every step.

VARA: What It Is and Who Needs It

What Is VARA?

The Virtual Assets Regulatory Authority (VARA) is the UAE’s specialized regulator for crypto, blockchain, and digital assets. Launched to bring structure to an emerging sector, VARA licenses only apply to businesses directly handling virtual assets.

Important distinction

VARA is not required for all fintech companies. If you’re building a traditional payment app, lending platform, or InsurTech solution, you don’t need VARA. You’ll use a standard business license instead.

Who Needs VARA Licensing?

You need VARA if your business involves:

- Crypto exchanges and trading platforms

- Digital wallet providers (custodial or non-custodial)

- DeFi protocols and yield farming platforms

- Stablecoin platforms and token issuance

- NFT marketplaces

- Blockchain-based payment solutions

- Tokenization services

Who Doesn’t Need VARA?

- Traditional payment processors

- Lending platforms (non-blockchain)

- Insurance technology solutions

- Compliance and RegTech platforms

- Cross-border payment services (non-crypto)

- AI-powered financial advisory tools

The Four VARA License Types

Understanding which license type fits your business model prevents costly delays. Here’s the breakdown:

| License Type | Best For | Regulatory Level | Capital Requirement | Timeline |

|---|---|---|---|---|

| Virtual Asset Exchange | Crypto trading platforms, exchanges | Highest | High | 8-12 weeks |

| Virtual Asset Wallet Provider | Digital wallets, custody services | Medium | Medium | 6-8 weeks |

| Virtual Asset Platform Operator | DeFi protocols, blockchain services | Medium-High | Medium | 7-10 weeks |

| Virtual Asset Advisor/Consultant | Crypto consulting, advisory | Lower | Low | 4-6 weeks |

Your Business Structure Options: Free Zones vs. Mainland

Choosing the right jurisdiction directly impacts your compliance burden, costs, and market access. Here’s your decision matrix:

Option 1: DMCC (Dubai Multi Commodities Centre)

Best for: Crypto and blockchain-focused businesses

DMCC is the most crypto-friendly free zone in the region. It has established infrastructure specifically for virtual asset companies and a proven track record with VARA licensing.

Cost Breakdown

- VARA License: AED 30,000 – 55,000 (annual)

- Office Space: AED 24,000 – 180,000 (depending on size)

- Team Visas (5 people): AED 14,500 – 20,500

- Professional Services: AED 10,000 – 20,000

- Total First Year: ~AED 80,000 – 275,000

Timeline: 4-6 weeks

Advantages

- Zero tax on qualifying income (under QFZP status)

- 100% foreign ownership allowed

- Dedicated fintech support team

- Proven regulatory relationship with VARA

Option 2: DIFC (Dubai International Financial Centre)

Best for: International-facing fintech, wealth management, investment technology

DIFC operates under common law jurisdiction, making it ideal for attracting global investors and clients familiar with UK/US regulatory frameworks.

Cost Breakdown

- VARA License: AED 38,000 – 75,000 (annual)

- Premium Office Space: AED 30,000 – 60,000

- Team Visas (5 people): AED 15,000 – 21,000

- Professional Services: AED 15,000 – 25,000

- Total First Year: ~AED 100,000 – 180,000

Timeline: 8-12 weeks

Advantages

- Common law jurisdiction (attracts international capital)

- DFSA (Dubai Financial Services Authority) reputation

- World-class infrastructure and networking

- Global fintech hub status

Option 3: Dubai Internet City / RAKEZ

Best for: Cost-conscious startups, traditional fintech (non-crypto)

These free zones offer the most affordable options while maintaining strong regulatory frameworks.

Cost Breakdown

- License: AED 20,000 – 30,000

- Office Space: AED 15,000 – 30,000

- Visas: AED 12,000 – 18,000

- Total First Year: ~AED 50,000 – 80,000

Timeline: 4-6 weeks

Option 4: Dubai Mainland

Best for: Traditional fintech requiring UAE-wide market access

Mainland companies can serve customers across the entire UAE without free zone restrictions.

Cost Breakdown

- License: AED 15,000 – 25,000

- Office: AED 20,000 – 40,000

- Visas: AED 15,000 – 20,000

- Total First Year: ~AED 50,000 – 85,000

Timeline: 6-8 weeks

The VARA License Application Process

Understanding the exact process prevents surprises and accelerates approval. The timeline typically spans 6-8 weeks.

Phase 1: Pre-Application (Weeks 1-2)

Step 1: Determine Your VARA License Type

Before submitting anything, clarify your business activity. Are you building a crypto exchange (Type 1), wallet provider (Type 2), DeFi platform (Type 3), or consulting service (Type 4)?

Choosing the wrong category causes unnecessary delays. Consult with a VARA-experienced legal advisor if you’re uncertain.

Step 2: Select Your Jurisdiction

Each free zone has different timelines and costs. Consider

- DMCC: Best crypto credibility, slightly higher cost

- DIFC: Premium international positioning, complex approval

- Dubai Internet City/RAKEZ: Budget-friendly, faster approval

Step 3: Prepare Core Documentation

Gather these before the formal application

- Detailed business plan (market size, revenue model, competitive advantage)

- Team credentials and experience

- Compliance framework outline

- Financial projections (3-5 years)

- Whitepaper (if blockchain-focused)

Phase 2: Application Submission (Weeks 2-4)

Step 4: Pre-Application with VARA

Submit preliminary documents to VARA. This helps identify gaps early and prevents rejection later.

Most applicants receive feedback within 1-2 weeks. Address any comments immediately.

Step 5: Formal VARA License Application

Submit a comprehensive application including

- Completed application forms

- Detailed business plan with market analysis

- Articles of Association

- Board composition and shareholder information

- AML/KYC policy documentation

- Cybersecurity and data protection framework

- Insurance details and coverage

- Professional references

- Financial statements or projections

Step 6: Compliance Interview

VARA conducts a regulatory panel meeting. Typically

- Present your business model and compliance approach

- Answer questions on AML/KYC procedures

- Discuss cybersecurity measures

- Technical deep-dive if applicable

Preparation is critical. Bring your compliance officer and any relevant technical experts.

Phase 3: Approval & Operations (Weeks 4-6+)

Step 7: Conditional Approval

Upon satisfactory interview, VARA issues conditional approval. This allows you to:

- Finalize office setup

- Deploy compliance systems

- Prepare for bank account opening

- Begin hiring

Step 8: License Issuance

Final license arrives after completing operational prerequisites.

Step 9: Bank Account Opening

Open a VARA-compliant business account. This typically takes 2-3 weeks. Required documents:

- VARA license

- Articles of Association

- Board resolutions

- Director identification

- Proof of office address

Crypto-friendly banks include First Abu Dhabi Bank (FAB), ADIB, and UAE Bank. Start conversations early—some require 3-4 weeks for approval.

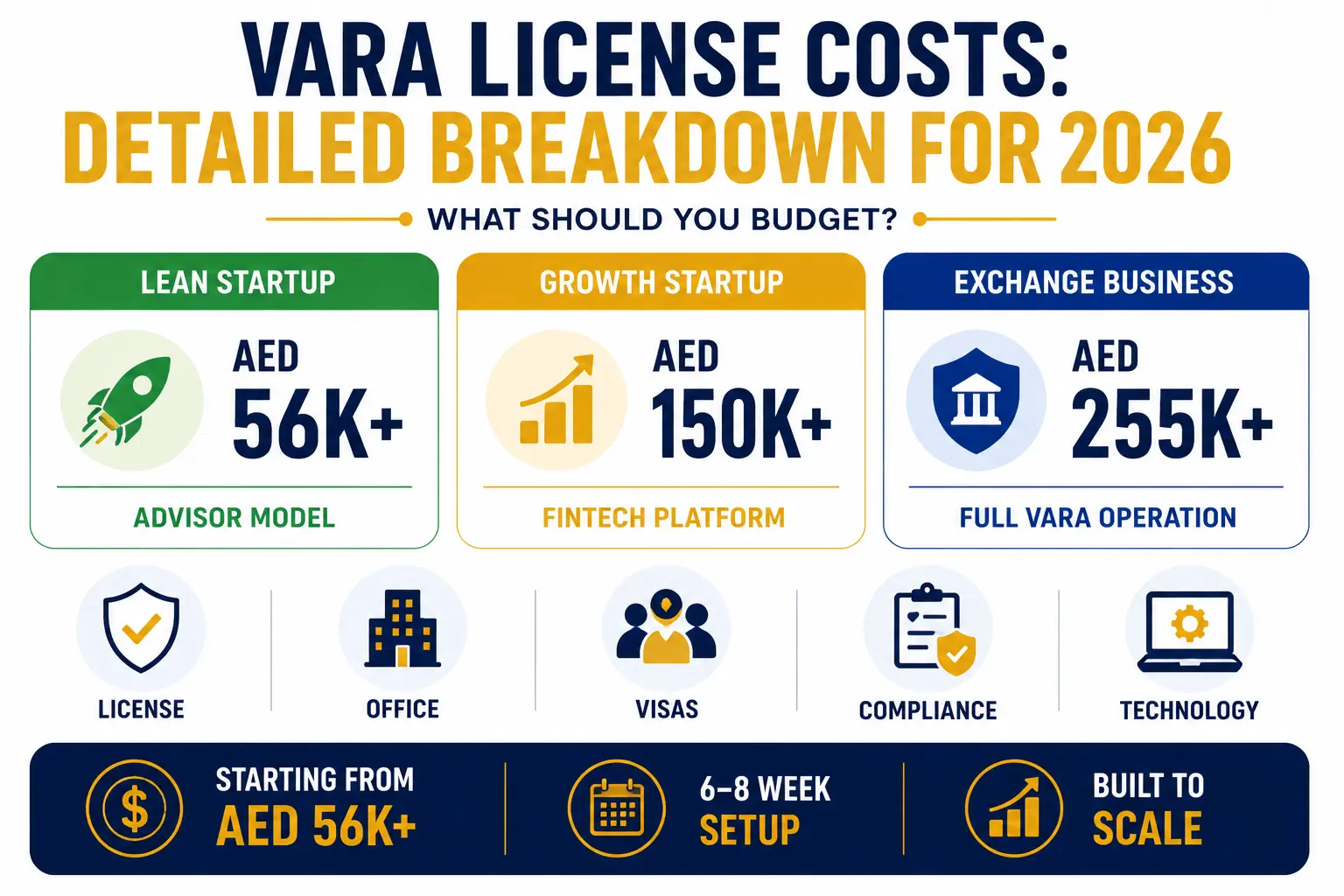

VARA License Costs: Detailed Breakdown For 2026

Understanding the true cost of setup prevents budget shocks.

VARA License Fees

| Fee Type | DMCC | DIFC | Dubai Internet City |

|---|---|---|---|

| Application Fee | AED 5,000 | AED 8,000 | AED 3,000 |

| Annual License Fee | AED 20,000-40,000 | AED 25,000-50,000 | AED 15,000-25,000 |

| Regulatory Fee | AED 5,000-10,000 | AED 5,000-15,000 | AED 2,000-5,000 |

| Total Year 1 | AED 30,000-55,000 | AED 38,000-75,000 | AED 20,000-33,000 |

Infrastructure & Operational Costs

Office Space

- Hot desk: AED 2,000-3,500/month (AED 24,000-42,000/year)

- Flexi-desk: AED 3,500-5,500/month (AED 42,000-66,000/year)

- Private office: AED 8,000-15,000/month (AED 96,000-180,000/year)

Technical Infrastructure

- AML/KYC software: AED 3,000-8,000/month (AED 36,000-96,000/year)

- Cybersecurity tools: AED 2,000-5,000/month (AED 24,000-60,000/year)

- Compliance platform: AED 1,500-3,000/month (AED 18,000-36,000/year)

Annual Tech Cost Range: AED 78,000-192,000

Team Visas & Immigration

Per person

- Visa application: AED 2,500-3,500

- Medical check: AED 300-500

- Emirates ID: AED 100

For a 5-person founding team: AED 14,500-20,500

Professional Services

- VARA application support: AED 10,000-20,000

- Compliance framework development: AED 5,000-10,000

- Legal documentation: AED 5,000-10,000

- Accounting setup: AED 2,000-5,000

Total First-Year Cost Scenarios

Lean Startup (Advisor/Consultant Model)

- VARA license: AED 30,000

- Virtual office: AED 10,000

- 1-2 team visas: AED 6,000

- Professional services: AED 10,000

- Total: approximately AED 56,000

Growth Setup (Crypto Exchange)

- VARA license: AED 50,000

- Office space: AED 60,000

- Technical infrastructure: AED 80,000

- Compliance platform: AED 30,000

- 3-4 team visas: AED 10,000

- Professional services: AED 25,000

- Total: approximately AED 255,000

Compliance & Ongoing Obligations: What VARA Requires

Compliance is not a one-time activity it is ongoing. VARA maintains strict standards to protect the ecosystem.

AML/KYC (Anti-Money Laundering/Know Your Customer)

Your compliance framework must include:

Customer Onboarding

- Enhanced due diligence (EDD) for high-risk customers

- Identity verification using government-approved methods

- Source of funds verification

- Politically exposed person (PEP) screening

Ongoing Monitoring

- Transaction monitoring systems

- Quarterly customer risk reassessment

- Suspicious activity flagging

Documentation

- Maintain 7-year record retention

- Complete transaction logs and audit trails

- Customer files and verification documents

- Compliance monitoring records

Cybersecurity & Data Protection

VARA requires security standards equivalent to ISO 27001

- Multi-factor authentication (MFA) for all user accounts

- Cold storage for cryptocurrency holdings

- Regular penetration testing (quarterly minimum)

- Incident response plan with 24-hour notification procedures

- GDPR-compliant data protection policies

Reporting & Audits

Regular Submissions

- Quarterly compliance reports to VARA

- Annual financial statements

- Annual compliance audit

- Suspicious activity reporting within 10 days

Regulatory Inspections

VARA conducts onsite inspections without notice to verify compliance. Preparation is essential.

Capital & Reserve Requirements

Minimums vary by license type

- Exchange Operators: Highest capital requirement (varies by assets under management)

- Wallet Providers: Moderate capital (typically AED 500,000+)

- Advisors/Consultants: Lower capital (AED 100,000+)

Additionally, maintain

- Operational reserve (6-12 months of expenses)

- Customer protection fund

- Comprehensive insurance coverage

Funding Your Fintech Startup In 2026

Government support and investor appetite are at all-time highs.

Government Incentives

VARA Fast-Track Program

Innovative fintech solutions receive expedited regulatory approval. Startups working on core infrastructure (payment rails, blockchain interoperability) qualify.

R&D Tax Credits

Qualify for 30-50% R&D tax deductions on qualifying technical development. This substantially reduces effective costs.

UAE Startup Grants

Up to AED 100,000 available for pre-revenue startups meeting criteria (innovation, team credentials, market potential).

D33 Agenda Support

The UAE’s national fintech strategy prioritizes:

- Government capital allocation for emerging fintech

- Tech incubator and accelerator access

- Regulatory fast-track for government-supported projects

Investor Landscape In MENA

Venture Capital

- Regional VCs establishing MENA-focused fintech funds

- Global firms opening regional offices (Polychain, Pantera)

- Typical check size: USD 100,000 – 2,000,000

- Focus: Seed to Series B stage

Angel Investors

- Tech entrepreneur networks investing in fintech

- High-net-worth individuals seeking MENA exposure

- Family offices allocating to emerging tech

Funding Timeline

Seed Round (Post-MVP)

- Amount: USD 100,000 – 500,000

- Timing: 3-6 months to close

- Metrics: Initial traction, engaged users, revenue model validation

Series A (Product-Market Fit)

- Amount: USD 500,000 – 3,000,000

- Timing: 4-8 months to close

- Metrics: Revenue, user base growth, unit economics

Series B (Scaling)

- Amount: USD 2,000,000 – 10,000,000+

- Timing: 6-10 months to close

- Metrics: Profitability trajectory, market leadership position

Success Factors: What Actually Works In Dubai’s Fintech Ecosystem

Building a fintech company is complex. These factors separate winners from those who struggle.

1. Clear Value Proposition

Successful fintech startups solve specific, measurable problems:

- Cross-border payments: Reducing remittance costs for MENA diaspora (typically 5-7% fees become 0.5-2%)

- Micro-lending: Serving underserved SMEs with faster approval than traditional banks

- Compliance automation: Simplifying regulatory requirements for regulated businesses

- Trade finance: Digitizing expensive, manual processes

Vague positioning (“we are building the fintech of the future”) fails. Specific solutions win funding and customers.

2. Regulatory Compliance From Day One

VARA-regulated companies that treat compliance as an afterthought fail inspections. Successful companies

- Build compliance into product architecture (not bolted on)

- Hire a dedicated compliance officer before launch

- Conduct quarterly internal audits

- Maintain transparent reporting with regulators

This approach builds investor confidence and protects your license.

3. Funding Strategy & Capital Planning

Successful startups do not just seek funding they plan it

- Map funding roadmap (seed → Series A → B)

- Mix funding sources (grants reduce dilution, VC accelerates growth)

- Leverage government programs (R&D credits, grants)

- Choose strategic investors with MENA network value

4. Regional Expansion Roadmap

MENA represents 400+ million people. Successful fintech companies

- Prove model in UAE first (6-12 months)

- Expand to GCC (Saudi Arabia, Kuwait, Bahrain) – similar regulations

- Then MENA-wide (Egypt, Morocco have growing fintech scenes)

- Eventually international (once proven at scale)

5. Technology & Security Excellence

User trust hinges on security. Invest in

- Best-in-class infrastructure (AWS, Google Cloud, or similar)

- Regular security audits (penetration testing quarterly)

- Zero-trust security architecture

- Continuous threat monitoring

This is not an optional insurance requirement; it mandates it.

Common Challenges & Solutions

Challenge 1: Regulatory Complexity

Reality: VARA requirements are stringent; compliance is expensive.

Solutions:

- Hire experienced compliance officer in first 90 days

- Budget AED 80,000-150,000 annually for compliance

- Work with VARA-experienced legal advisors (not general corporate lawyers)

- Join fintech associations for peer guidance and regulatory updates

Challenge 2: High Initial Costs

Reality: Total first-year setup ranges from AED 56,000 to AED 255,000+.

Solutions:

- Start with advisor/consultant model (lower cost, upgrade later)

- Use virtual office initially, upgrade as you grow

- Partner with compliance providers (shared infrastructure reduces costs)

- Hire lean initially, scale with revenue

Challenge 3: Talent Acquisition

Reality: Fintech talent is scarce; competition from established firms is intense.

Solutions:

- Offer equity compensation (startup equity appeals to risk-takers)

- Provide visa sponsorship and relocation support

- Consider remote team for non-compliance roles

- Partner with universities for intern pipelines

Challenge 4: Bank Account Opening

Reality: Some banks remain hesitant to work with crypto companies despite the VARA regulation.

Solutions:

- Work with crypto-friendly banks (FAB, ADIB, UAE Bank)

- VARA license dramatically improves banking relationships

- Apply for corporate banking packages (higher limits, faster processing)

- Start conversations 3-4 weeks before license issuance

Your Path Forward In Dubai’s Fintech Revolution

The opportunity before fintech founders in Dubai in 2026 is genuine and time-sensitive. This is not hype or speculation. The facts are clear.

The Reality Check

You now understand the complete fintech licensing landscape. You know the costs (AED 56,000 to AED 255,000+), the timeline (6-8 weeks), the compliance requirements, and the funding landscape. You have read about successful models and critical pitfalls to avoid.

But knowledge alone does not build companies. Action does.

The founders reading this guide fall into three categories:

Category 1: The Ready

You have a validated business model, a team, and capital ready to deploy. You understand the regulatory requirements and are prepared to move immediately. For you, the path is clear: choose your free zone, assemble your compliance framework, and submit your VARA application this month. Every week of delay costs opportunity.

Category 2: The Prepared

You have a strong idea, early customer interest, and some funding. You need clarity on the exact process and costs before committing. This guide has provided that. Your next step is consulting with a VARA-experienced legal advisor (2-3 weeks), then launching your application. Six months from now, you will either have your license and be operationally live, or you will be watching competitors scale while you wonder why you delayed.

Category 3: The Exploring

You are interested in fintech but uncertain about your specific model, team composition, or market fit. You are still in the research phase. This guide has helped you understand what is possible and what is required. Your action item is single: pick a specific problem to solve in the MENA fintech market, build an MVP or proof of concept, and validate customer demand. Once you have that validation, revisit this guide. The regulatory path will still be here, and you will be ready to execute.

Why Dubai, Why Now

Three factors create a unique window that will not remain open indefinitely.

- First, regulatory clarity arrived in 2025-2026. VARA is established. The path is defined. Early movers benefit from an operating environment that is still relatively uncrowded. In two years, when Dubai becomes widely recognized as the MENA fintech capital, applications will increase, approval timelines will stretch, and talent competition will intensify. Founders who launch now have advantages that founders launching in 2028 will not.

- Second, government support is active and real. The UAE’s D33 agenda prioritizes fintech. R&D tax credits exist today. Startup grants are available today. Accelerator programs are accepting applications today. These are not permanent benefits. Political priorities shift. Economic circumstances change. What exists today may not exist in 2027.

- Third, investor capital is flowing into MENA fintech. Regional VCs have established funds. Global investors are opening offices. The sentiment is positive. This investor appetite creates an unusual window where ideas that might struggle to raise funding in other markets can attract serious capital here. That dynamic also will not last forever. Investors are cyclical.

The founders who recognize this window and act during it will build the regional fintech giants of the 2030s. The founders who hesitate, research endlessly, and delay will watch from the sidelines.

The Investment You Are Making

Setting up your fintech company in Dubai requires investment across three dimensions.

Capital investment is clear. You are spending AED 56,000 to AED 255,000+ in your first year. This is not trivial for bootstrapped founders. But consider the alternative: building the same company in New York costs 10-15 times more. Building in London is similar. Building in Singapore is comparable. Dubai represents a capital-efficient jurisdiction for launching a world-class fintech operation.

Time investment is significant. You will spend 2-3 months on the VARA application process, compliance framework development, and regulatory engagement. This is time not spent on product development or customer acquisition. Plan for it. Allocate a team member to regulatory compliance (often the founder or a co-founder). Do not treat it as a distraction; treat it as a core strategic initiative.

Organizational investment matters most. Hiring a compliance officer early is not optional. Building AML/KYC processes into your product architecture from day one is not an afterthought. Treating regulatory obligations as core to your operations (not something bolted on later) separates companies that thrive from those that encounter licensing challenges. Make this cultural choice explicitly.

The Critical Success Factor You Cannot Skip

One factor above all others determines whether your fintech company succeeds or fails: clarity on who you are solving problems for and what problems you are solving.

Successful fintech companies address specific pain points:

Cross-border remittances cost 5-7% through traditional channels

SMEs cannot access credit from traditional banks

Trade financing requires weeks of manual documentation

Regulatory compliance consumes 10-15% of operational costs for regulated businesses

Unsuccessful fintech companies chase vague ideas:

“We are building the future of finance”

“Our blockchain solution will disrupt everything”

“We are like Stripe but for the MENA region”

Regulatory authorities notice this distinction immediately. Investors notice within 10 minutes. Customers notice when they evaluate whether your solution actually improves their operations.

Before you invest in VARA licensing, before you rent office space, before you hire your first employee, ensure you can articulate your value proposition in a single sentence that a non-technical person understands. If you cannot, keep developing your idea. If you can, move forward with confidence.

Your Next Action (This Week)

Do not finish reading this guide and close the tab.

Take one of these three actions this week

- Action 1: Schedule a consultation with a VARA-experienced legal advisor. Come prepared with your business model, team information, and timeline. Ask specific questions about your regulatory path. Get expert feedback on your approach. Cost: AED 2,000-5,000. Timeline: Schedule this week, meet next week.

- Action 2: Connect with at least three founders who have launched fintech companies in Dubai in the past 12 months. Ask them directly about their experience, costs, timeline, and lessons learned. Most founders are generous with guidance. These conversations will provide ground truth that no guide (including this one) can match.

- Action 3: Draft your business plan and compliance framework outline. Do not wait for perfect conditions. Work with what you have. Outline your business model, identify your target customer, define your regulatory path, and project your costs. Share this draft with your co-founders and get feedback.

Pick one. Start this week. Do not wait for perfect conditions. Perfect conditions do not exist. Founders who move during conditions that are 70% clear succeed. Founders who wait for 100% clarity never move.

Final Words

Dubai’s fintech opportunity in 2026 is real. The regulatory environment is supportive. The capital is available. The market is massive (400+ million people in MENA). The technology is proven.

What is rare is founder execution. Most people read guides like this and do nothing. They bookmark it, intending to take action “next month.” They consult with advisors but never submit applications. They have ideas but never validate them.

You are reading this because you are different. You are not passively wondering about fintech. You are actively researching how to build a fintech company. That disposition curiosity combined with action orientation—is the primary predictor of success.

The regulatory path is clear. The costs are defined. The timeline is realistic. The support systems exist.

The only remaining variable is you.

Will you be the founder who reads this guide, takes action, and builds the next regional fintech giant? Or will you be the founder who reads this guide, bookmarks it, and wonders two years from now why you did not move when the window was open?

The choice is yours. The time to decide is now.